.png)

For most Independent Software Vendors (ISVs), the primary focus is shipping features and growing Monthly Recurring Revenue (MRR) through software subscriptions. While this builds a solid foundation, relying solely on subscription fees ignores a massive lever for company valuation. You are leaving money on the table every time a customer processes a transaction outside of your ecosystem.

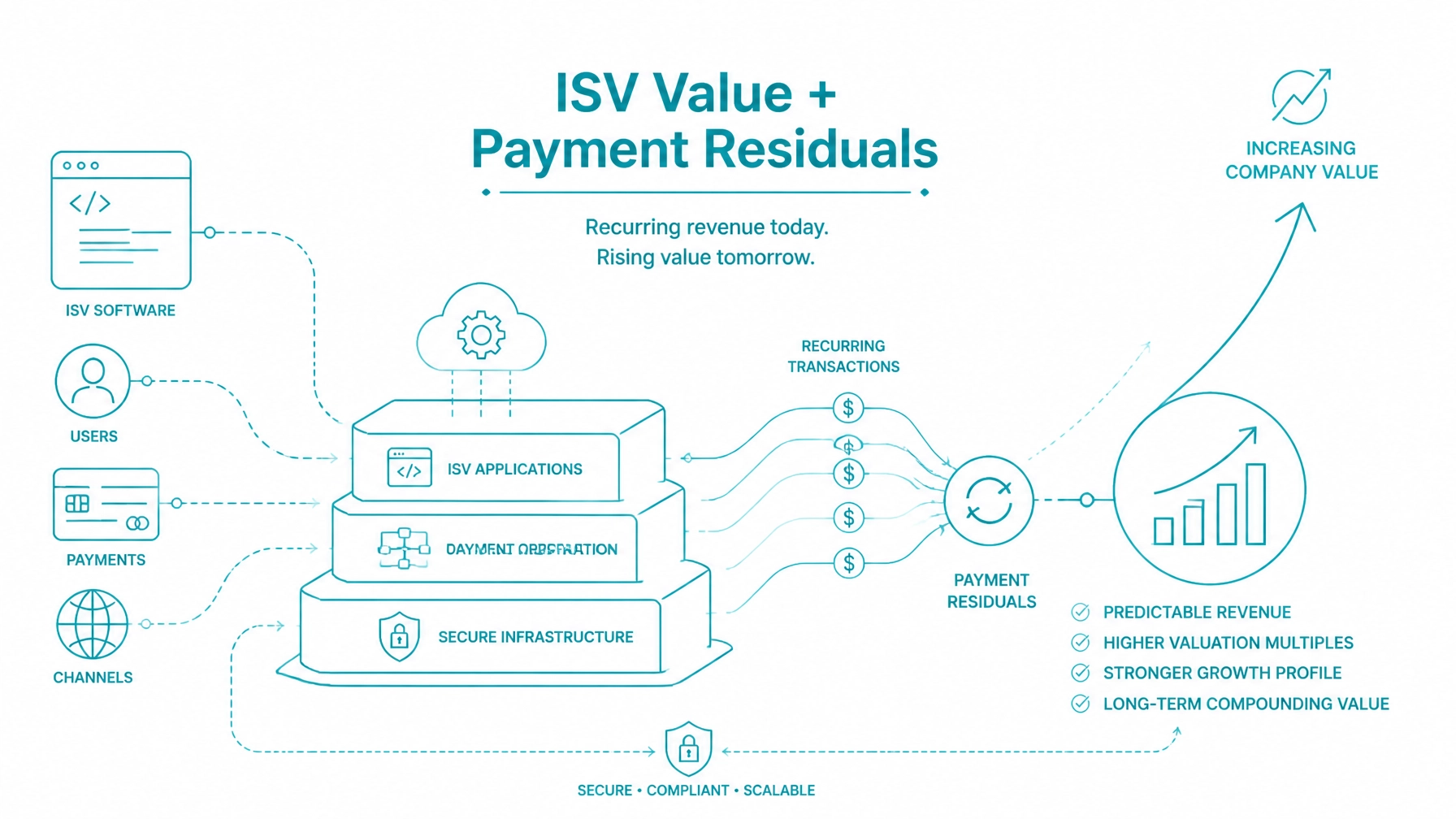

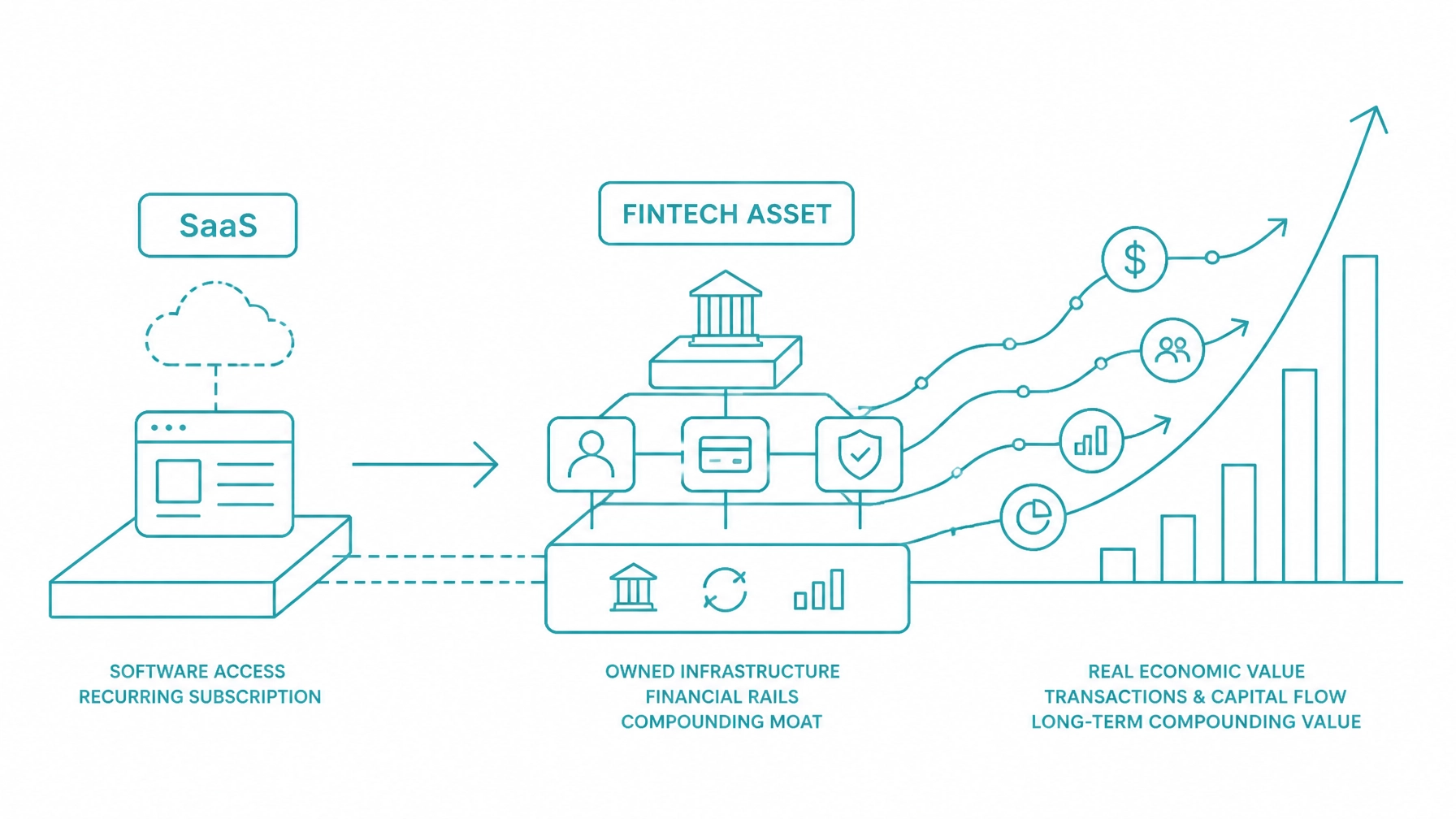

To build a high-value software company in today’s market, you must transition from being a simple SaaS provider to a fintech-enabled powerhouse. This shift happens through integrated payments. By embedding processing directly into your platform, you stop being a cost center and start building a portfolio of residual income.

This strategy does more than just add a few bucks to the bottom line. It creates a "second business" within your software that investors and acquirers value at much higher multiples than traditional service revenue.

The difference between a $10 million company and a $50 million company often comes down to how much of the transaction flow they capture. When you integrate payments, you are no longer just selling a tool; you are facilitating the entire financial life cycle of your users.

Traditional SaaS revenue is predictable, but it is also susceptible to churn and competition. Payment residuals, however, are tied directly to your customers' cash flow. As their business grows, your revenue grows automatically without you needing to upsell a single additional seat or feature.

This transition turns your software into a fintech asset. Acquirers look for "stickiness." When a merchant relies on your software to run their business and your gateway to get paid, the cost of switching becomes prohibitively high. This increased retention drastically boosts your valuation multiples.

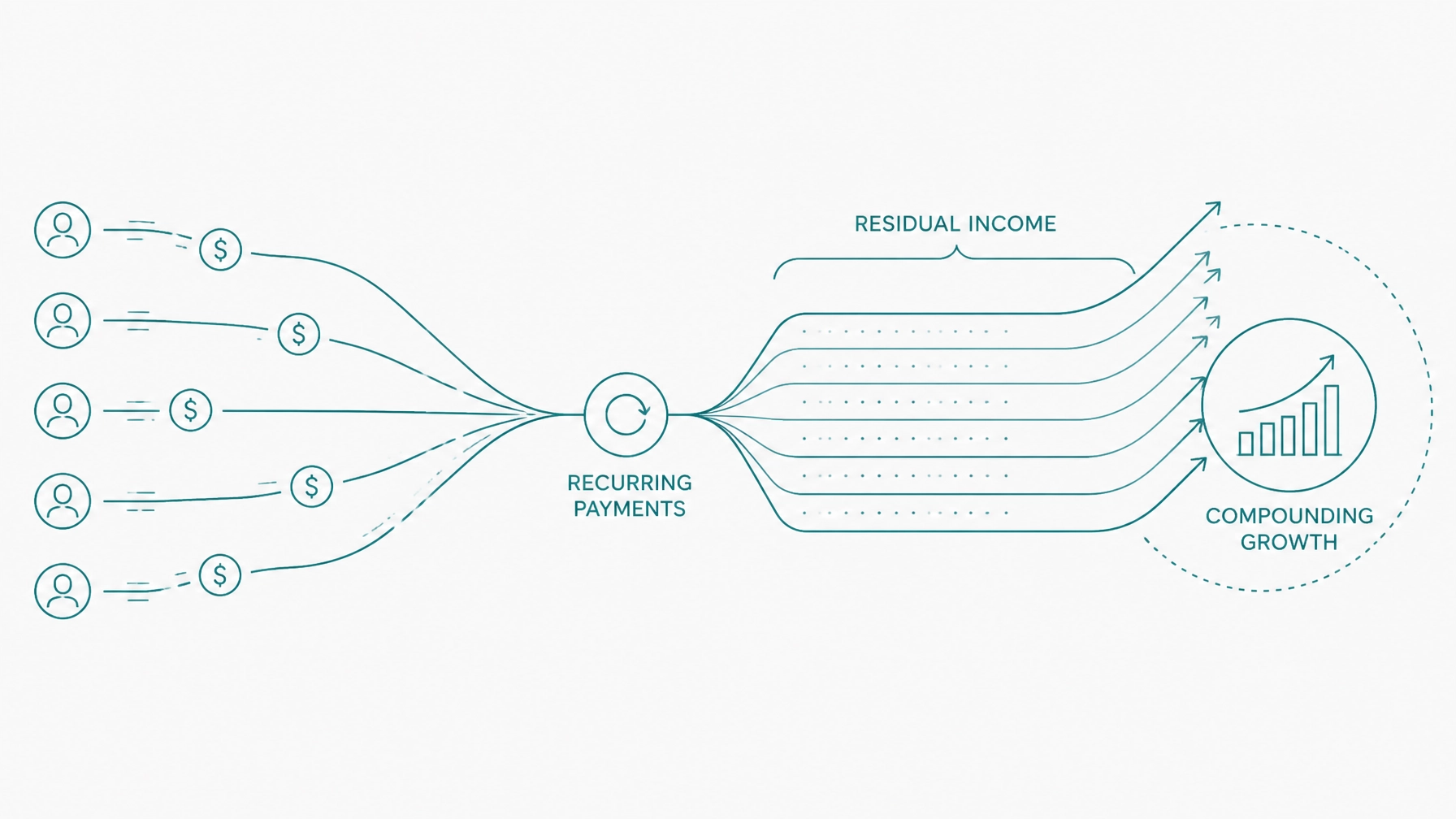

Residual income in the payment world is the "spread" or commission you earn on every transaction processed through your integration. Unlike one-time referral fees, residuals pay out every single month for the life of the merchant account.

By maximizing residual income as an independent merchant services agent or software partner, you are essentially building a pension for your company. A well-managed portfolio of processing clients can be sold for 25x to 40x its monthly value as a standalone asset.

If your software processes $100 million in annual volume and you capture a modest 20 basis points (0.20%) in residual margin, that is $200,000 in pure, high-margin profit. In the eyes of a Private Equity firm, that revenue is often more attractive than subscription revenue because it scales linearly with economic activity.

Investors value "quality of earnings." They want to see revenue that is recurring, high-margin, and scalable. Integrated payments check all three boxes. When an ISV builds a payment portfolio, they are creating a diversified stream of income that buffers against market volatility.

Acquirers typically apply a higher multiple to payment revenue because it represents a "take rate" on the overall industry your software serves. For example, if you build software for medical practices, you aren't just betting on your software; you're taking a piece of the entire healthcare spending flow handled by your clients.

This makes your company an attractive acquisition target for larger fintech firms, banks, or competitors looking to consolidate market share. You aren't just selling code; you're selling a pre-built, revenue-generating financial network.

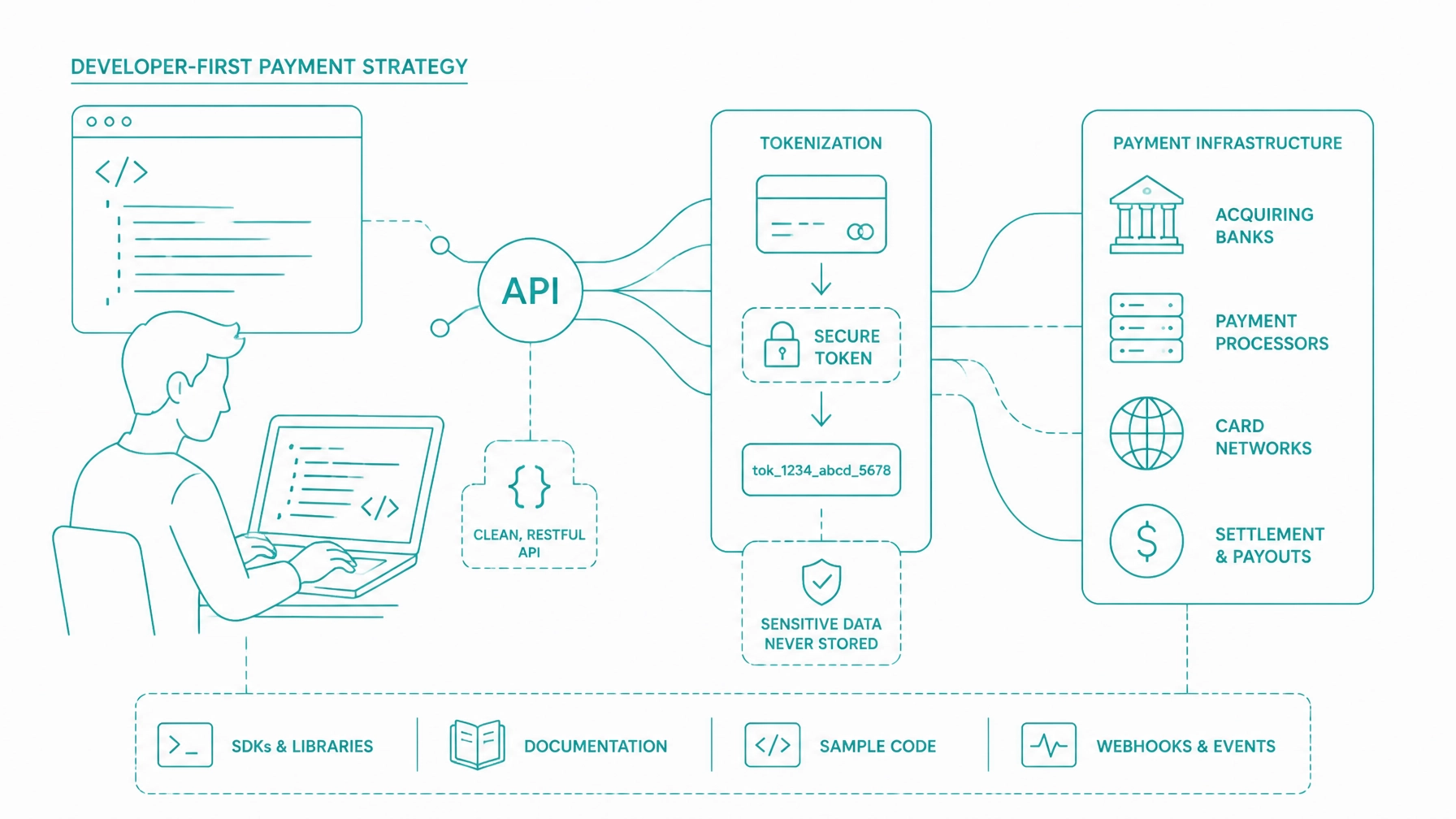

Success in this space requires more than just slapping a "pay now" button on a checkout page. It requires a deliberate technical strategy. You need a partner that allows you to own the customer experience while they handle the heavy lifting of moving money.

When scaling custom web applications, your payment strategy must be flexible enough to handle various merchant needs. Whether your clients need recurring billing payments API for custom software or physical hardware in a retail setting, your integration must be seamless.

Integrate Payments provides the infrastructure that allows ISVs to scale without the headache of building a full payment stack from scratch. This allows your team to focus on core product features while the residual checks keep rolling in.

Your engineering team is your most valuable resource. If you force them to work with clunky, legacy payment systems, you’ll face delays and bugs that stifle growth. A developer-first payment API is essential for rapid deployment.

Modern APIs should offer:

When your developers can integrate quickly, you get to market faster. The faster you get to market, the sooner you start building your residual portfolio.

Many startups begin with Stripe because it’s easy to set up. However, as an ISV looking to maximize company value, Stripe’s flat-fee model is often a disadvantage. Stripe typically keeps the entire margin, leaving the software vendor with zero residual income or a very thin "platform fee."

When comparing Integrate Payments vs. Stripe, the difference becomes clear at scale. Integrate Payments allows you to participate in the transaction spread. Instead of giving away the most profitable part of the transaction to a third party, you keep it for yourself.

Over time, this difference in revenue can mean millions of dollars in additional valuation during an exit. Own the integration, own the data, and most importantly, own the revenue.

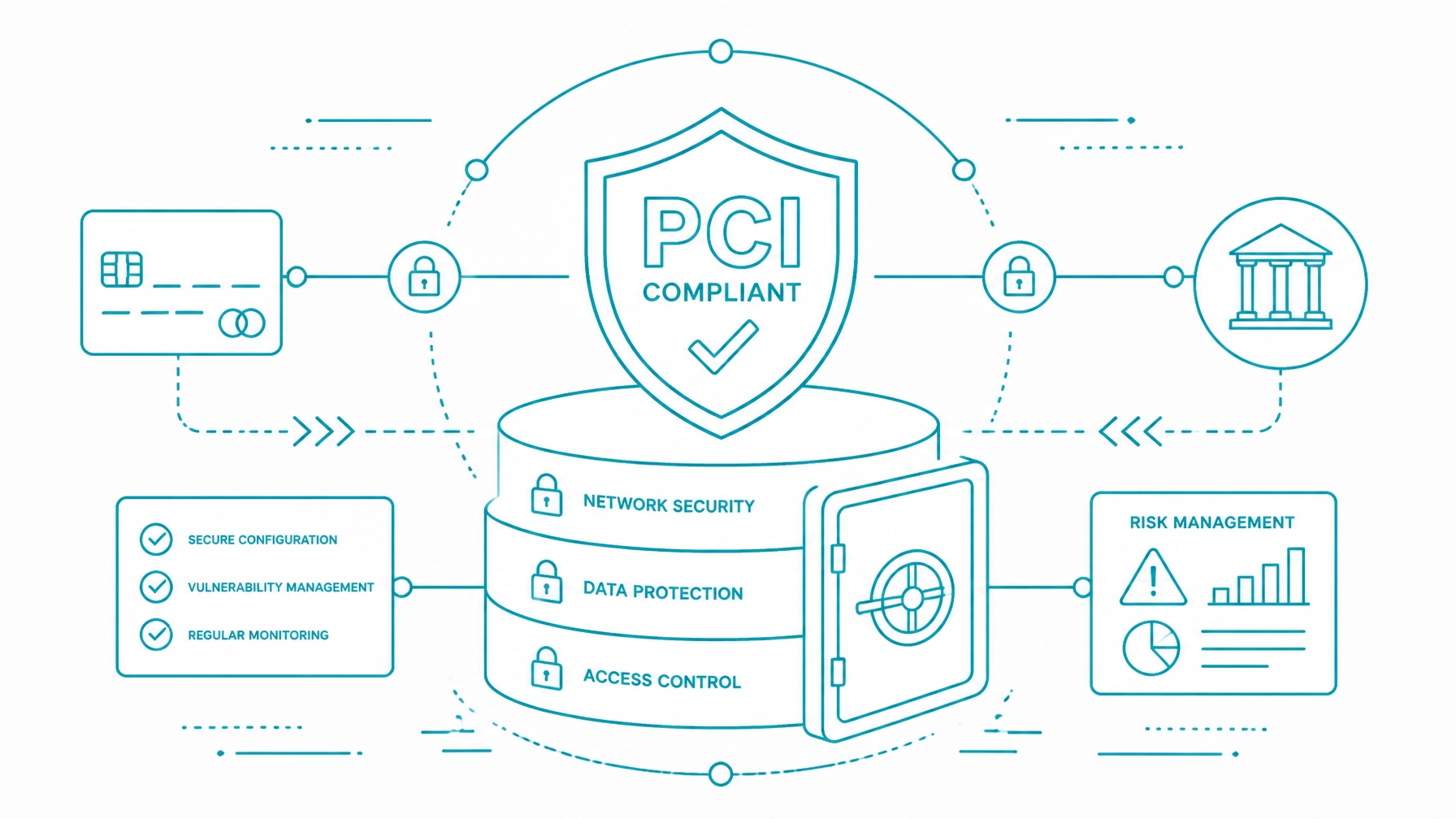

Building a high-value company also means protecting that value. Security and compliance are not optional. If your platform suffers a data breach, your valuation will plummet instantly.

By using advanced security features like a secure credit card info customer vault, you can provide a "one-click" checkout experience for your users without actually storing raw credit card data. This significantly reduces your scope for PCI audits.

Learning how to become PCI compliant is a critical step for any ISV. A compliant, secure platform is a much safer bet for investors, and it ensures that your residual portfolio remains a stable, long-term asset.

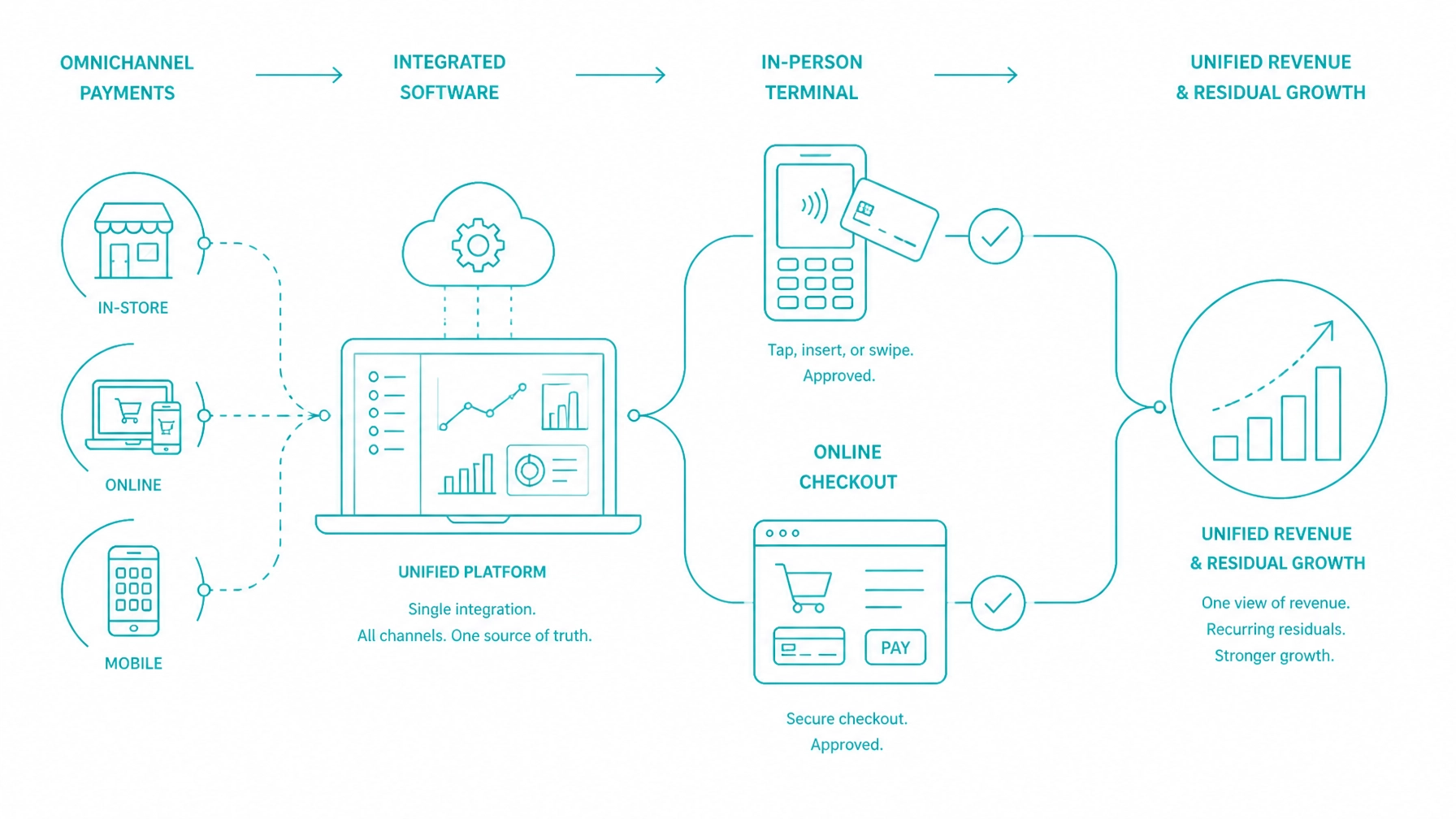

Integrated payments aren't limited to e-commerce. If your software serves brick-and-mortar businesses, you can capture residuals from physical card swipes as well. Offering integrated point of sale equipment allows you to own the entire merchant experience.

When a merchant buys their hardware and software from you, they are "locked in." This omnichannel approach: combining web, mobile, and in-person payments: creates the most valuable type of residual portfolio because it captures 100% of the merchant's processing volume.

The goal is simple: transform your ISV from a product company into a platform company. By building a portfolio of residual-producing clients, you create a self-sustaining revenue engine that works while you sleep.

Every new customer you sign up doesn't just increase your MRR; they increase the size of your fintech asset. This dual-track growth: subscription plus residuals: is the fastest way to maximize the value of your company.

Don't let the payment processors take the lion's share of the value you created. Use Integrate Payments to build your own portfolio, secure your transactions, and scale your company to its highest possible valuation.

Integrate Payments provides the tools, APIs, and partnership models needed to help ISVs succeed in the modern fintech landscape. Whether you are building the next big e-commerce platform or a niche vertical SaaS, integrated payments are the key to your long-term wealth.