Selecting a credit card processing pricing model is a foundational decision for any SaaS company or high-growth merchant. The choice between flat rate and interchange plus directly impacts your bottom line and financial reporting clarity.

For developers building payment logic, the underlying pricing structure influences how data is reconciled within your application. Understanding these two frameworks ensures that your platform remains profitable as transaction volumes scale.

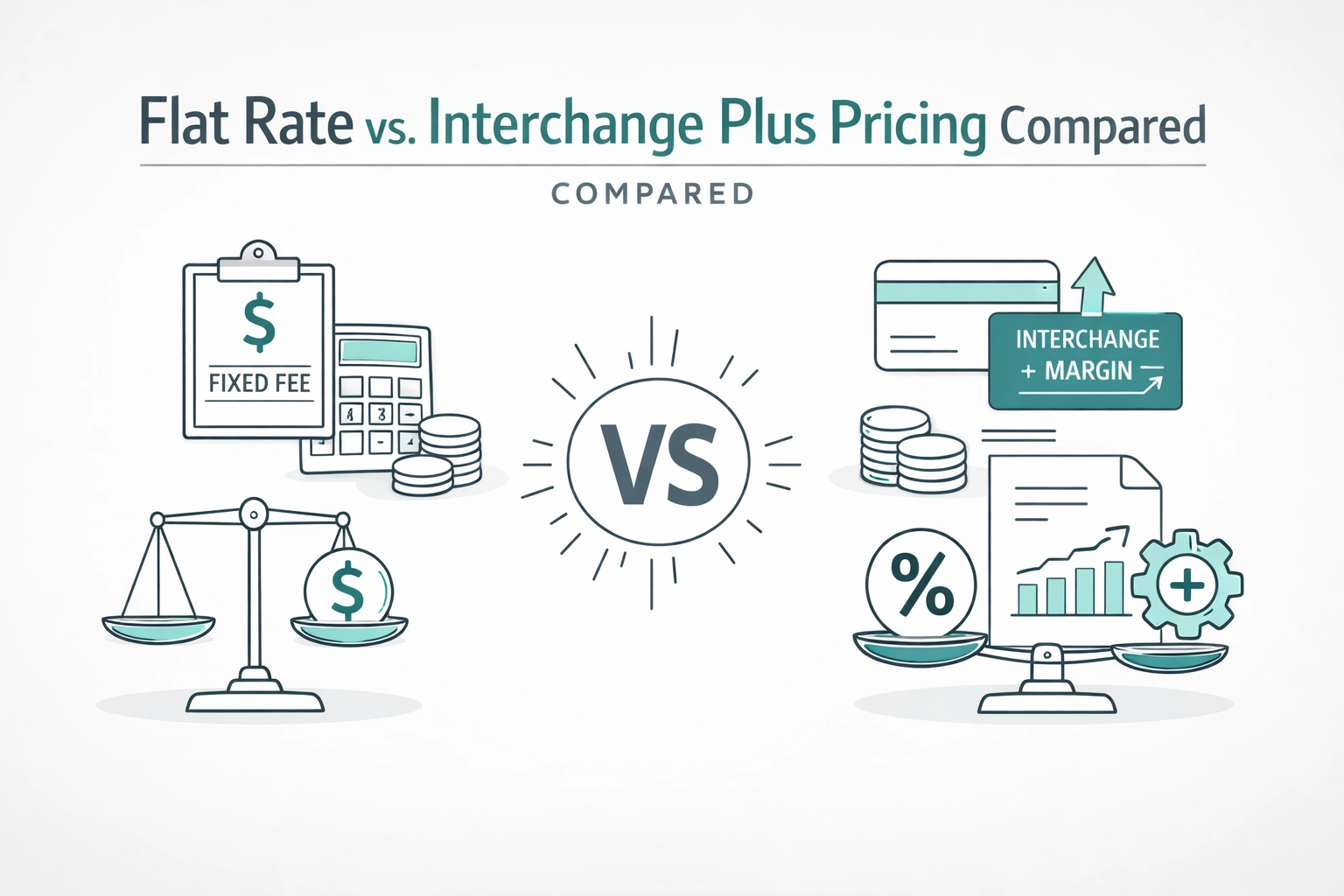

Flat rate pricing is a simplified model where the merchant pays a fixed percentage and a flat fee for every transaction. This structure is commonly associated with payment aggregators that prioritize quick onboarding and ease of use.

In this model, all transaction types are treated the same regardless of the card used or the level of risk involved. Whether a customer uses a basic debit card or a high-reward corporate credit card, the cost to the merchant remains identical.

A typical flat rate structure often looks like this:

2.9% + $0.30 per transaction.

While this predictability is helpful for startups with low monthly volumes, it often masks the true cost of processing. The processor keeps the difference between their flat rate and the actual cost set by the card networks.

Interchange plus is often referred to as cost-plus pricing. It is the gold standard for transparency in the fintech industry and is the preferred choice for established SaaS platforms and high-volume merchants.

This model separates the processing costs into three distinct components. First is the interchange fee, which is the non-negotiable rate set by card brands like Visa and Mastercard.

The second component is the assessment fee paid directly to the card networks. The third is the processor's markup, which is the only negotiable part of the equation.

By using an interchange pass-through cost plus pricing program, merchants see exactly what the card networks charge. This level of granularity is essential for businesses that need to audit their financial health.

SaaS companies often operate on tight margins where every basis point matters. Using a flat rate model for high-volume processing can result in thousands of dollars in "lost" margin every month.

Interchange plus allows SaaS founders to capture the savings associated with lower-cost transactions. For example, a standard debit card carries a much lower interchange rate than a premium rewards card.

Under a flat rate model, the processor pockets the savings from that debit card transaction. Under interchange plus, those savings stay with the merchant.

Integrate Payments provides the tools necessary for SaaS platforms to implement these transparent structures. You can view our gateway and processor pricing to see how we help businesses move beyond the limitations of flat-rate models.

Developers responsible for payment integrations must consider how pricing affects the developer experience. While the API calls may remain the same, the reporting requirements differ significantly.

Flat rate models offer simple reporting because every transaction has the same fee logic. However, they lack the data depth required for sophisticated financial dashboards.

Interchange plus provides the raw data needed to build detailed cost-analysis tools for your users. Utilizing a developer sandbox allows teams to test how these different fee structures appear in transaction logs.

For a merchant processing $5,000 a month, the simplicity of a flat rate model may outweigh the potential savings of interchange plus. The overhead of managing a merchant account might not be worth the $50 in savings.

However, as a company grows toward $50,000 or $100,000 in monthly volume, the math shifts. A 2.9% flat rate on $100,000 is $2,900 in fees plus transaction costs.

An interchange plus model might average out to 2.10% total including the markup. On that same $100,000, the merchant pays $2,100, saving $800 every single month.

These savings scale linearly with your growth. For large-scale marketplaces and platforms, these savings are often used to fund further development or customer acquisition.

Pricing is not just about the percentage per transaction. Indirect costs, such as non-compliance fees and security overhead, can significantly impact your effective rate.

Many flat-rate providers do not offer hands-on assistance with security requirements. This can lead to unexpected monthly "non-compliance" fees that are buried in your statement.

Integrate Payments simplifies PCI compliance and secure credit card storage. By using our hosted tools, you reduce your compliance scope and avoid unnecessary financial penalties.

Our hosted website checkout options ensure that sensitive data never touches your server. This technical approach reduces the risk of data breaches while keeping your processing costs low.

There is a common misconception that interchange plus is harder to integrate. In reality, the integration complexity depends on the quality of the payment API, not the pricing model.

Integrate Payments offers a robust omnichannel payment platform that supports interchange plus pricing without adding code complexity. You get the benefit of lower costs with the same ease of integration found in flat-rate providers.

Whether you are integrating Authorize.net or using our proprietary SDKs, the focus remains on technical efficiency. You should not have to choose between a good API and a fair price.

Flat rate pricing is an appropriate starting point for specific business stages. New businesses with no processing history often find it easier to get approved for flat-rate aggregator accounts.

If your monthly volume is consistently under $5,000, the time spent managing a full merchant account might exceed the financial savings. It is a "starter" model designed for convenience over cost-efficiency.

Once your business establishes a history of consistent processing, moving to an interchange plus model becomes a logical step for financial optimization.

The transition to interchange plus should occur when your business seeks to professionalize its financial operations. This is often triggered by reaching a volume milestone or when preparing for a funding round where margins are scrutinized.

Businesses that process a high volume of B2B or debit transactions will see the most immediate benefit. These card types have lower interchange rates that flat-rate models simply cannot match.

Integrate Payments assists merchants in making this transition seamlessly. We provide the merchant account services and the point of sale terminal equipment needed to handle transactions across all channels.

For SaaS founders, payments should be a profit center, not a cost center. Selecting the right pricing model is the first step in optimizing your payment stack.

Avoid being locked into high flat rates by choosing a partner that offers scalability. Integrate Payments supports your growth from the first transaction to enterprise-level volume.

By focusing on transparency and developer-first tools, we ensure that your payment integration is an asset to your growth. Start by exploring our sitemap to find the specific integration tools and pricing programs that fit your current business needs.

Integrate Payments provides secure and reliable payment processing solutions for businesses of all sizes. Our services are designed to help you streamline your payment operations and grow your business. For more information about our services and how we can help you, please contact us today. All merchant accounts are subject to credit approval. All terms and conditions apply.